Compare car insurance quotes online free sets the stage for a journey into the world of saving money on your car insurance. This process can be both empowering and rewarding, allowing you to secure the best coverage at the most affordable price.

Table of Contents

Navigating the complex world of car insurance can be daunting, but understanding the basics and utilizing the right tools can make all the difference. By comparing quotes from multiple insurers, you gain valuable insights into the market and discover potential savings that may have otherwise gone unnoticed.

The Importance of Comparing Car Insurance Quotes

In today’s competitive insurance market, it’s more important than ever to shop around and compare car insurance quotes before settling on a policy. This can save you hundreds or even thousands of dollars per year.

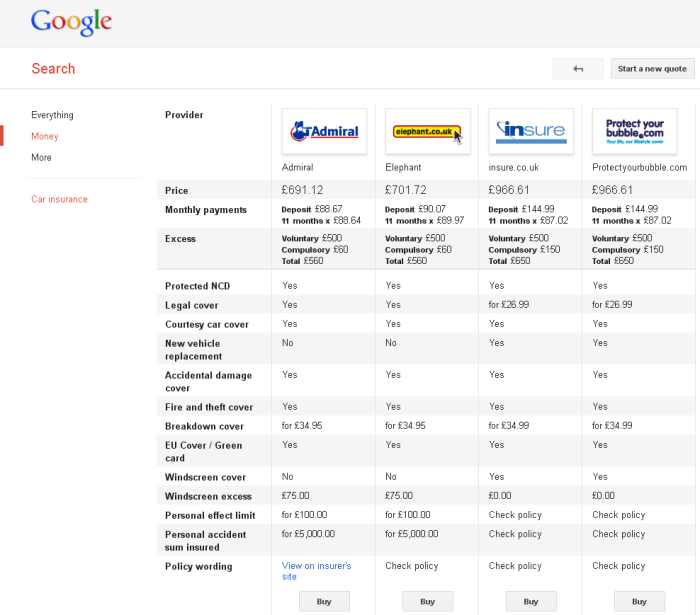

Comparing car insurance quotes online can be a quick and easy way to find the best coverage at the most affordable price. You can easily compare quotes from multiple insurers in just a few minutes. This allows you to see the different coverage options available, the premiums charged, and the discounts offered by each insurer.

Potential Savings by Comparing Quotes

Comparing car insurance quotes can help you find significant savings. By comparing quotes, you can often find lower premiums than what you’re currently paying. For example, a recent study found that drivers who switched to a new insurer after comparing quotes saved an average of $500 per year.

“The average driver can save $500 per year by comparing car insurance quotes and switching to a new insurer.”

Understanding Car Insurance Quotes

Before you can compare car insurance quotes, it’s important to understand what they represent and the factors that influence their pricing. Car insurance quotes are estimates of how much you’ll pay for coverage. They are based on a variety of factors, including your driving history, the type of vehicle you drive, and your location.

Key Terms, Compare car insurance quotes online free

Car insurance quotes use specific terminology to describe the different components of your coverage. Here’s a breakdown of some key terms:

- Premium: The amount you pay for your car insurance policy. It is typically paid monthly or annually.

- Deductible: The amount you pay out of pocket before your insurance company starts covering the costs of an accident or other covered event. A higher deductible generally means a lower premium, and vice versa.

- Coverage: The types of events or damages your insurance policy will cover. Different types of coverage have different limits and exclusions.

Types of Car Insurance Coverage

Car insurance policies typically offer several types of coverage to protect you and your vehicle in different situations.

- Liability Coverage: This coverage protects you financially if you cause an accident that injures another person or damages their property. It covers the other driver’s medical expenses, lost wages, and property damage up to the policy limits. Liability coverage is usually required by law in most states.

- Collision Coverage: This coverage pays for repairs or replacement of your vehicle if it’s damaged in a collision with another vehicle or object, regardless of fault. It covers the cost of repairs or replacement, minus your deductible.

- Comprehensive Coverage: This coverage protects your vehicle against damage from non-collision events, such as theft, vandalism, fire, hail, or natural disasters. It covers the cost of repairs or replacement, minus your deductible.

- Uninsured/Underinsured Motorist Coverage: This coverage protects you if you’re injured in an accident caused by an uninsured or underinsured driver. It covers your medical expenses, lost wages, and property damage up to the policy limits.

- Personal Injury Protection (PIP): This coverage covers your medical expenses and lost wages if you’re injured in an accident, regardless of who is at fault. It is typically required in no-fault states.

Factors Influencing Insurance Costs

Several factors contribute to the cost of your car insurance premiums.

- Driving History: Your driving record, including accidents, traffic violations, and DUI convictions, significantly impacts your premiums. Drivers with a clean record generally pay lower premiums than those with a history of accidents or violations.

- Vehicle Type: The type of vehicle you drive also influences your premiums. Luxury cars, sports cars, and high-performance vehicles are generally more expensive to insure than standard vehicles due to their higher repair costs and potential for greater damage.

- Location: Your location can affect your premiums due to factors such as traffic density, crime rates, and weather conditions. Areas with higher traffic congestion or higher crime rates often have higher insurance premiums.

- Age and Gender: Younger drivers and drivers of certain genders may face higher premiums due to statistical data suggesting higher risk factors in these groups.

- Credit Score: In some states, insurance companies may consider your credit score when determining your premiums. A higher credit score generally means lower premiums.

Choosing the Right Online Comparison Tool: Compare Car Insurance Quotes Online Free

Navigating the world of car insurance can feel overwhelming, but with the right tools, you can find the best coverage at the most competitive price. Online comparison websites are a fantastic resource for simplifying the process, but choosing the right one is crucial.

Reputable Online Comparison Websites

When choosing a comparison tool, it’s essential to consider its reputation, features, and user experience. Several reputable websites stand out for their comprehensive coverage and user-friendly interfaces.

- Compare.com: This website boasts a vast network of insurance providers, allowing you to compare quotes from multiple companies simultaneously. Its user-friendly interface makes it easy to navigate and customize your search.

- The Zebra: The Zebra prides itself on its extensive data analysis and personalized recommendations. It provides detailed insights into each insurance policy, helping you make an informed decision.

- Insurify: This website excels in its ability to compare quotes from a wide range of insurance providers, including those that might not be readily available elsewhere.

- Policygenius: Policygenius is known for its transparent and unbiased approach. It offers personalized recommendations based on your individual needs and preferences.

- NerdWallet: NerdWallet is a comprehensive financial resource that includes a robust car insurance comparison tool. It offers detailed insights into each policy, making it easier to understand the differences between options.

Key Features to Consider

Each online comparison tool offers a unique set of features, so it’s essential to identify the features that are most important to you.

- Quote Accuracy: The accuracy of the quotes provided is paramount. A reputable comparison tool will use real-time data from insurance providers to ensure the quotes are up-to-date and accurate.

- Ease of Use: A user-friendly interface makes the comparison process straightforward. Look for websites with clear navigation, intuitive search filters, and easy-to-understand policy details.

- Coverage Options: The comparison tool should allow you to compare quotes for various coverage options, including liability, collision, comprehensive, and uninsured/underinsured motorist coverage.

- Customer Service: It’s always a good idea to choose a comparison tool with excellent customer service. Look for websites that offer live chat support, phone assistance, and helpful FAQs.

- Privacy and Security: Ensure the comparison tool you choose takes data security seriously. Look for websites that use encryption technology to protect your personal information.

Comparing and Contrasting Tools

Once you’ve identified a few comparison tools that meet your basic needs, it’s time to compare and contrast them based on specific factors.

- Ease of Use: Compare the user interface of each tool. Consider the clarity of navigation, the availability of search filters, and the overall user experience.

- Quote Accuracy: Check the accuracy of the quotes provided by each tool. Compare the quotes to those offered directly by insurance providers to ensure consistency.

- Customer Service: Test the customer service of each tool by asking questions or submitting inquiries. Evaluate the responsiveness, helpfulness, and overall satisfaction with the support provided.

- Additional Features: Compare the additional features offered by each tool, such as policy analysis, discounts, and personalized recommendations.

Recommendations

While all the websites listed above are reputable, some might be better suited to your specific needs. For example, if you prioritize ease of use and a wide range of insurance providers, Compare.com might be the best choice. If you value personalized recommendations and detailed policy insights, The Zebra could be a better option.

Ultimately, the best way to choose the right online comparison tool is to try out a few different options and see which one best meets your needs. Take advantage of free trials or demo versions to get a feel for each tool before committing.

Tips for Getting Accurate Quotes

Getting accurate car insurance quotes is crucial for finding the best deal. Providing correct and complete information is essential for a personalized quote that reflects your specific needs and risk profile.

Essential Information Checklist

To receive accurate quotes, you need to provide the following information:

- Your personal details: This includes your name, address, date of birth, and contact information.

- Driving history: This includes your driving license number, years of driving experience, any accidents or violations, and your driving record.

- Vehicle information: This includes the make, model, year, and VIN (Vehicle Identification Number) of your car.

- Coverage details: You need to specify the type of coverage you need, such as liability, collision, comprehensive, and uninsured/underinsured motorist coverage.

- Other relevant factors: This may include your annual mileage, parking location, and whether you have any safety features in your vehicle.

Being Honest and Transparent

It’s important to be honest and transparent when providing information about your driving history and vehicle.

“Lying about your driving record or vehicle details could result in your insurance being canceled if you make a claim.”

If you have a history of accidents or violations, it’s best to be upfront about it. This will allow insurers to accurately assess your risk and provide you with a quote that reflects your driving history.

Avoiding Common Mistakes

Here are some common mistakes to avoid when getting car insurance quotes:

- Not comparing quotes from multiple insurers: Different insurers have different pricing structures and may offer better rates for specific profiles. Comparing quotes from multiple insurers can help you find the best deal.

- Using outdated information: Make sure the information you provide is up-to-date. If you’ve recently moved, changed your vehicle, or had your driving record updated, ensure you reflect these changes in your quote request.

- Not understanding the different types of coverage: Different types of coverage offer varying levels of protection. It’s important to understand the different types of coverage and choose the one that best suits your needs.

- Not considering optional coverage: Optional coverage, such as roadside assistance or rental car reimbursement, can provide additional protection and peace of mind. Consider your needs and budget when deciding whether to add these options.

Understanding Your Policy

You’ve compared quotes, chosen the best insurance plan, and are ready to hit the road. But before you do, it’s crucial to understand your policy inside and out. Your car insurance policy is a legal contract that Artikels the terms and conditions of your coverage. Taking the time to read and understand your policy can help you avoid costly surprises and ensure you’re getting the protection you need.

Coverage Details

This section Artikels the specific types of coverage you have and their limits. For example, you’ll find information about your liability coverage, collision coverage, comprehensive coverage, and uninsured/underinsured motorist coverage.

- Liability coverage: This protects you financially if you cause an accident that injures someone or damages their property. It covers the other driver’s medical expenses, lost wages, and property damage.

- Collision coverage: This covers damage to your vehicle if you’re involved in an accident, regardless of who is at fault.

- Comprehensive coverage: This covers damage to your vehicle from events other than accidents, such as theft, vandalism, or natural disasters.

- Uninsured/underinsured motorist coverage: This protects you if you’re injured in an accident caused by a driver who doesn’t have insurance or doesn’t have enough insurance to cover your losses.

Exclusions

This section details what your policy doesn’t cover. Understanding the exclusions can help you avoid surprises when you need to file a claim. For example, most policies exclude coverage for damage caused by wear and tear, mechanical breakdowns, or driving under the influence.

Claims Procedures

This section Artikels the steps you need to take to file a claim. It will explain how to report an accident, what information you need to provide, and the process for getting your claim reviewed and approved.

Tips for Navigating Your Policy

- Read your policy carefully: Don’t just skim the document. Take your time and read it thoroughly, paying attention to the details.

- Ask questions: If you don’t understand something, don’t hesitate to contact your insurance agent or company.

- Keep your policy in a safe place: You’ll need easy access to your policy if you need to file a claim.

- Review your policy regularly: Your needs may change over time, so it’s a good idea to review your policy at least once a year to ensure it still meets your needs.

Factors Affecting Car Insurance Costs

Your car insurance premium is determined by various factors, each contributing to the overall cost. Understanding these factors can help you make informed decisions to potentially lower your premium.

Factors Influencing Car Insurance Costs

Here’s a breakdown of key factors affecting your car insurance costs:

| Factor | Description | Impact on Premium | Examples |

|---|---|---|---|

| Age | Younger drivers are statistically more likely to be involved in accidents, leading to higher premiums. | Higher for younger drivers, lower for older drivers. | A 20-year-old driver may pay significantly more than a 40-year-old driver with a similar driving record. |

| Driving History | A clean driving record with no accidents or violations results in lower premiums. | Lower for drivers with no accidents or violations, higher for drivers with accidents or violations. | A driver with multiple speeding tickets will likely pay more than a driver with no violations. |

| Vehicle Type | The type of vehicle you drive, including its make, model, and safety features, influences your premium. | Higher for expensive, high-performance, or less safe vehicles. | A luxury sports car will generally cost more to insure than a basic sedan. |

| Location | Your location, including the state, city, and neighborhood, impacts your premium. | Higher in areas with higher crime rates, traffic congestion, or a greater risk of natural disasters. | A driver living in a major city may pay more than a driver in a rural area. |

| Credit Score | In some states, insurers consider your credit score as a proxy for risk assessment. | Higher for drivers with lower credit scores. | A driver with excellent credit may qualify for lower premiums than a driver with poor credit. |

| Coverage Options | The type and amount of coverage you choose, such as liability limits, collision coverage, and comprehensive coverage, affect your premium. | Higher for more comprehensive coverage and higher liability limits. | A driver with higher liability limits will generally pay more than a driver with lower limits. |

| Deductible | The amount you’re willing to pay out of pocket in case of an accident, known as the deductible. | Higher deductible means lower premium, lower deductible means higher premium. | A driver with a $1000 deductible will likely pay less than a driver with a $500 deductible. |

| Driving Habits | Factors like mileage driven, driving distance, and time of day you drive can influence your premium. | Higher for drivers with high mileage, long commutes, or who drive during peak hours. | A driver who commutes long distances daily may pay more than a driver who primarily drives short distances. |

Saving Money on Car Insurance

Finding the cheapest car insurance rates is great, but there are ways to save even more money on your premiums. By taking a proactive approach and making some adjustments, you can significantly reduce your annual costs.

Improving Your Driving Record

A clean driving record is a key factor in determining your insurance rates. Maintaining a safe driving history can lead to significant savings.

- Avoid Traffic Violations: Every traffic violation, from speeding tickets to parking violations, can increase your premiums. Even minor offenses can add up over time.

- Defensive Driving Courses: Taking a defensive driving course can demonstrate your commitment to safe driving and often earns you a discount on your insurance.

- Avoid Accidents: Accidents are the biggest factor in increasing your insurance rates. Drive defensively and be aware of your surroundings to minimize the risk of accidents.

Increasing Your Deductible

Your deductible is the amount you pay out-of-pocket before your insurance coverage kicks in. A higher deductible generally means lower premiums.

- Consider Your Risk Tolerance: A higher deductible means you’ll pay more if you have an accident, so consider your financial situation and risk tolerance when deciding.

- Example: If your current deductible is $500 and you increase it to $1000, you might see a 10-15% reduction in your premium. However, you’ll be responsible for paying the first $1000 of any claim.

Bundling Insurance Policies

Many insurance companies offer discounts when you bundle multiple policies, such as car insurance, homeowners insurance, or renters insurance.

- Potential Savings: Bundling can save you 10-20% or more on your premiums, depending on the insurer and the policies you bundle.

- Shop Around: Compare quotes from different insurers to see which offers the best bundle discounts.

Negotiating with Insurers

Don’t be afraid to negotiate with your insurer to try and get a lower rate.

- Loyalty Discounts: Ask about loyalty discounts if you’ve been with the same insurer for a long time.

- Payment Options: Inquire about discounts for paying your premium annually or semi-annually instead of monthly.

- Other Discounts: See if you qualify for other discounts, such as good student discounts, safe driver discounts, or discounts for installing anti-theft devices in your car.

Additional Resources and Information

This section provides you with valuable resources and information to help you understand car insurance better. We’ll explore government websites, insurance industry organizations, and consumer protection agencies.

Government Websites and Insurance Industry Organizations

Government websites and insurance industry organizations offer valuable resources and information about car insurance.

- National Association of Insurance Commissioners (NAIC): The NAIC is a non-profit organization that works to promote uniformity in state insurance laws. Their website offers information on various insurance topics, including car insurance, and provides links to state insurance departments.

- Insurance Information Institute (III): The III is a non-profit organization that provides information about insurance and risk. Their website offers educational materials, statistics, and research on car insurance.

- Federal Trade Commission (FTC): The FTC is a federal agency that protects consumers from unfair and deceptive business practices. Their website offers information on how to avoid insurance scams and file complaints.

- State Insurance Departments: Each state has its own insurance department that regulates the insurance industry within that state. These departments can provide information on car insurance requirements, consumer protection, and complaint resolution.

Consumer Protection Agencies and Insurance Regulators

Consumer protection agencies and insurance regulators play a vital role in protecting consumers and ensuring fair insurance practices.

- Consumer Financial Protection Bureau (CFPB): The CFPB is a federal agency that protects consumers in the financial marketplace. Their website offers resources on car insurance, including information on your rights and how to file complaints.

- State Insurance Departments: As mentioned earlier, each state has its own insurance department that regulates the insurance industry within that state. These departments can provide information on car insurance requirements, consumer protection, and complaint resolution.

Recommended Books, Articles, and Online Resources

There are numerous books, articles, and online resources available that can help you gain a deeper understanding of car insurance.

- “The Complete Idiot’s Guide to Car Insurance” by James A. Lee: This book provides a comprehensive guide to car insurance, covering topics such as choosing the right coverage, understanding your policy, and saving money.

- “Car Insurance for Dummies” by Mary Beth Quaranto: This book offers a straightforward and easy-to-understand guide to car insurance, covering essential aspects of the topic.

- “Car Insurance: A Consumer’s Guide” by the National Association of Insurance Commissioners (NAIC): This guide provides valuable information on car insurance, including coverage options, choosing the right policy, and filing claims.

- “How to Get the Best Car Insurance Rates” by Consumer Reports: This article offers practical tips on how to save money on car insurance, including comparing quotes, negotiating rates, and understanding your policy.

- “Car Insurance: What You Need to Know” by NerdWallet: This article provides a comprehensive overview of car insurance, covering topics such as coverage options, factors affecting rates, and finding the best deals.

Legal and Regulatory Considerations

Understanding the legal framework governing car insurance is crucial for both consumers and insurers. This ensures fair practices, consumer protection, and a stable insurance market.

Role of Insurance Regulators

Insurance regulators play a vital role in protecting consumers by setting standards, enforcing laws, and resolving disputes. They ensure that insurance companies operate fairly and responsibly, providing adequate coverage and handling claims efficiently.

Common Insurance Scams and How to Avoid Them

Insurance scams can take various forms, and being aware of them can help you avoid falling victim. Here are some common scams and tips to protect yourself:

- Fake Insurance Companies: Be cautious of companies that seem too good to be true, offering extremely low premiums. Verify the legitimacy of the company through official regulatory websites or by contacting your state insurance department.

- Phishing Scams: Never click on suspicious links or provide personal information over the phone or email without verifying the source.

- Fake Accident Claims: If you’re involved in an accident, be wary of individuals who claim to be injured but show no signs of injury. Report any suspicious activity to the police and your insurance company.

- Inflated Repair Costs: Get multiple estimates for repairs and compare them to ensure you’re not being overcharged.

The Future of Car Insurance

The car insurance industry is undergoing a significant transformation, driven by advancements in technology, data analytics, and the emergence of autonomous vehicles. These developments are shaping the way insurance is priced, how coverage is provided, and ultimately, how consumers interact with their insurance providers.

The Impact of Technology and Data Analytics

Technology and data analytics are playing a pivotal role in reshaping the car insurance landscape.

- Telematics: Telematics devices, often integrated into smartphones or connected car systems, collect data on driving behavior, such as speed, braking, and mileage. This information allows insurers to assess risk more accurately and offer personalized premiums based on individual driving habits. For example, a driver with a consistently safe driving record might receive a lower premium compared to someone with a history of risky driving behavior.

- Artificial Intelligence (AI): AI algorithms are being used to analyze vast amounts of data, including driving records, claims history, and even weather patterns, to predict future risks and personalize insurance quotes. This enables insurers to offer more competitive rates and tailor coverage to individual needs.

- Data-Driven Pricing: The use of data analytics allows insurers to move away from traditional risk assessment models based on demographics and towards more dynamic pricing models that consider individual driving behavior and risk profiles. This shift is leading to more accurate and fair pricing, as premiums are based on actual driving habits rather than broad generalizations.

Empowered with knowledge and armed with the right tools, you can confidently navigate the car insurance landscape and secure the best coverage for your needs. By taking the time to compare quotes online, you can unlock significant savings and ensure that you are adequately protected on the road. Remember, your car insurance is a vital financial safety net, and understanding its intricacies is crucial for financial peace of mind.

Comparing car insurance quotes online can save you time and money. You can easily get multiple quotes from different insurance companies, allowing you to find the best coverage at the most competitive price. Remember, insurance coverage is crucial, so take a look at auto coverage quotes to understand the different types available. By taking the time to compare quotes online, you can ensure you’re getting the best value for your money on your car insurance.